How to lose a lot of money

Why the "student debt issue" is a lot worse than you think

My student loan balance is incorrect. I suspect that thousands of other loan balances are also incorrect. A few weeks ago, I noticed this discrepancy — that my qualifying federal student loans had not only been accruing interest during Covid’s infamous interest-free period, but had been accruing a mathematically incorrect amount of interest based on the interest rate described — and I emailed my loan servicer, Nelnet.

A few days later, I received a reply which stated very quickly that interest did not accrue during the period I described, because that was impossible. Exactly like Kafka, I looked at the $700+ interest charges which had accumulated on my account since March 2020, imagined the bureaucracy I needed to fight, and woke up the next morning as a beetle. My spindly appendages were helpful in googling what the hell was going on with student loan servicers. (It turns out: more than you’d think.)

On Monday the New York Times described a beautiful economy: “President Biden and his aides are basking in what is arguably the best run of economic data to date in his presidency. Inflation is cooling, business investment is rising, [and] job growth is powering on.” The article later concedes “polls still show Mr. Biden remains underwater on his handling of the economy.” Some economists might act puzzled, but it doesn’t seem like a single mom waiting for the price of eggs to drop beneath $2.50 would have noticed marginal improvements in various macroeconomic indicators.

Moreso, if you’re one of the hundreds of thousands of people whose payments start sometime in October, you are about to experience a sudden, extreme economic shock mostly ignored by these indicators. The shock might even be celebrated for its deflationary effects. Whether you went to Harvard Law and now earn a $250k corporate law base salary or you’re a sociology master’s student at the University of Phoenix doing humble nonprofit work for pennies, the bill that’s about to hit you (and your credit report) is astonishing.

While the left and right spent the months leading up to the Supreme Court’s student loan decision passionately debating whether or not people with student loans could afford yachting in St. Tropez, Biden’s student loan team was busy cooking up basically nothing. The White House’s new student loan strategy is pretty weak, especially considering the months of lead time in advance of the Supreme Court’s decision. To get out of this situation, the Department of Education may have been able to issue a Final Rule and/or Biden could have enacted subsequent Executive Orders, which would have represented a real attempt at solving the crisis. Instead, the new strategy will take over a year to implement, and will likely face the same legal concerns as the initial (thwarted) attempt.

Plenty of people may tell you the student loan crisis doesn’t matter. They might even think it’s like a tax on the rich. And I sort of see where they’re coming from – it’s a luxury only 14% of the population has — that gives them, by definition, better jobs — so why bother? They signed up for the loans. They probably got good jobs. Let them deal.1

But if you dig just a little deeper, the whole “student loan issue” gets thorny. People didn’t know what they were getting into. Loans sound cheap at 6%, but they’re not when spread over a lifetime. People entered fields where a graduate degree was the best – or only – entry point, and didn’t have a choice in the matter. People were heavily marketed to, from LinkedIn to Instagram, promised deals on tuition and career outcomes that never materialized. So much of the modern immigration system for smart young people is tied to education, forming a system where international students essentially can enroll for a short visa but must enter a complicated lottery for a longer-term visa that allows them to stay and work.

Not to mention, hedge fund endowments with teaching programs attached, sorry I mean top universities, hungry for cash cow Master’s programs, rapidly scaled their programs when they realized federal loans had fewer and fewer strings attached. A $20k Master’s program for 20 students per class could be an $80k Master’s program for 200 students if you just sold it a little harder.

Twenty-two year-olds across the nation didn’t understand what was happening and thought, hey, I want a career in Sociology or Legal Studies or Art History, and this seems to be what you do to get one. So they signed up for more debt they will ever reasonably be able to pay back in their lifetime, because we let the system get away with it, requiring minimal to no checks on student outcomes. In fact, we encouraged the system. When limits on GradPLUS loans were relaxed in 2006 by a Republican-controlled Congress, many hoped access to graduate education would be expanded. Instead, economists have found the opposite – tuition got more expensive and students borrowed more, but the demographics of the student population largely stayed the same.

Only the tragedy doesn’t end there. Then many of these people were promised a significant haircut on their debt – $10k or $20k – enough to radically reshape their household finances – which evaporated a year later.

Ultimately, the industries that incentivize it, the programs that incentivize it, and the culture of more education equals better personhood all contribute to a world where ambitious young people get screwed. There was a brief cultural moment when the Administration acknowledged this. A moment where the $10k forgiven might have led to something more – an acknowledgement that the situation had spiraled out of control and the time had come to start fixing it – starting with the people most impacted, people with low salaries and ballooning interest, and out from there – and then the period ended.

Biden has revised some rules; I’m sure he had several dozen Millennial staffers eager to revise the Public Interest Student Loan Forgiveness program, which used to exist in name and not work in practice, which may now work in both. But clearly we’ve given up on what will doom the many future generations of young people, letting a balloon grow and grow – and instead of popping it, just letting it float away.

All of this writing and I haven’t even gotten to the servicers themselves, who are some of the worst actors in the entire system. While incredible advances have been made since 2010 (prior to which, public student loans were held by private entities), servicers continue to fail Americans in unique ways while they earn money off the backs of students. Before the pandemic, servicers were known for brazenly breaking laws. Now, they’re completely unprepared for the payments to come.

Most recently, one of the largest student loan servicers, Navient, was sued by several State Attorney Generals for violating the Fair Credit Reporting Act and the Fair Debt Collection Act, two acts I would consider important not to violate. In the moderate words of the Consumer Financial Protection Bureau, Navient was “systematically and illegally failing borrowers at every stage of repayment.” Among many, many other complaints, the servicer became notorious for attempting to collect debts from co-signers after its student debtors’ accidental deaths, violating its own policy not to do that. After having been sued many times, Navient finally ended its contract with the Department of Education in 2021. 44% of public borrowers were then shifted to other servicers, potentially with “new” (i.e., incorrect) student loan balances.

Since the pandemic began, two other servicers ended their contracts with the Department of Education, Granite State and PHEAA. Granite State’s contract was not renewed after dozens of formal complaints were received by the CFPB and the Better Business Bureau, including trouble with payments, incorrect information provided about loans, problems with customer service, and inflexibility about loan repayment options. PHEAA mismanaged its contracts so poorly that Senate Democrats called for an official investigation amid other lawsuits, including from the State of California, as borrowers were not able to access the student loan relief they were legally entitled to.

There are only eight student loan servicers in the Federal Student Aid program remaining: Great Lakes Educational Loan Services, Edfinancial, MOHELA, Aidvantage, Nelnet, OSLA Servicing, ECSI, and the Default Resolution Group. I suspect that, in the confusion of the post-pandemic repayment restart, they will have similar fates. Payments to servicers are due in two months, and at least in my own case, my servicer hasn’t bothered to formally calculate my monthly payment yet. Sites will crash. Staffs are ill-equipped. People will pay back balances which aren’t their own. As more servicers crash and burn, the students beholden to them will reenter the endless maze of repayment, with new entities to pay and new risks of getting swindled.

Just today, Nelnet released the monthly payment amounts for many of its borrowers, prompting the customer call center to, you guessed it, crash. This student loan restart is unprecedented and it will not be smooth.

I am as sick of the “avocado toast-loving millennials” narrative as the “all student debtors are PhDs in underwater basketweaving” narrative. Even if you focus on the degree itself, plenty of MBAs, the Internet Right’s favorite graduate degree, go into societally-valuable nonprofit or under-paid public sector work after graduation and struggle to pay back their loans. These beliefs just hinder policy addressed at helping young people.

Only groups like the Debtor’s Collective seem to be taking matters seriously. Their innovative structure – a literal union of debtors – is one of few groups seriously challenging the harms of the status quo. Like the observations David Graeber makes in Debt, we should ultimately interrogate our cultural understandings of debt and repayment, and why we assume that debts, especially those taken on in bad circumstances, need to be paid back at all.

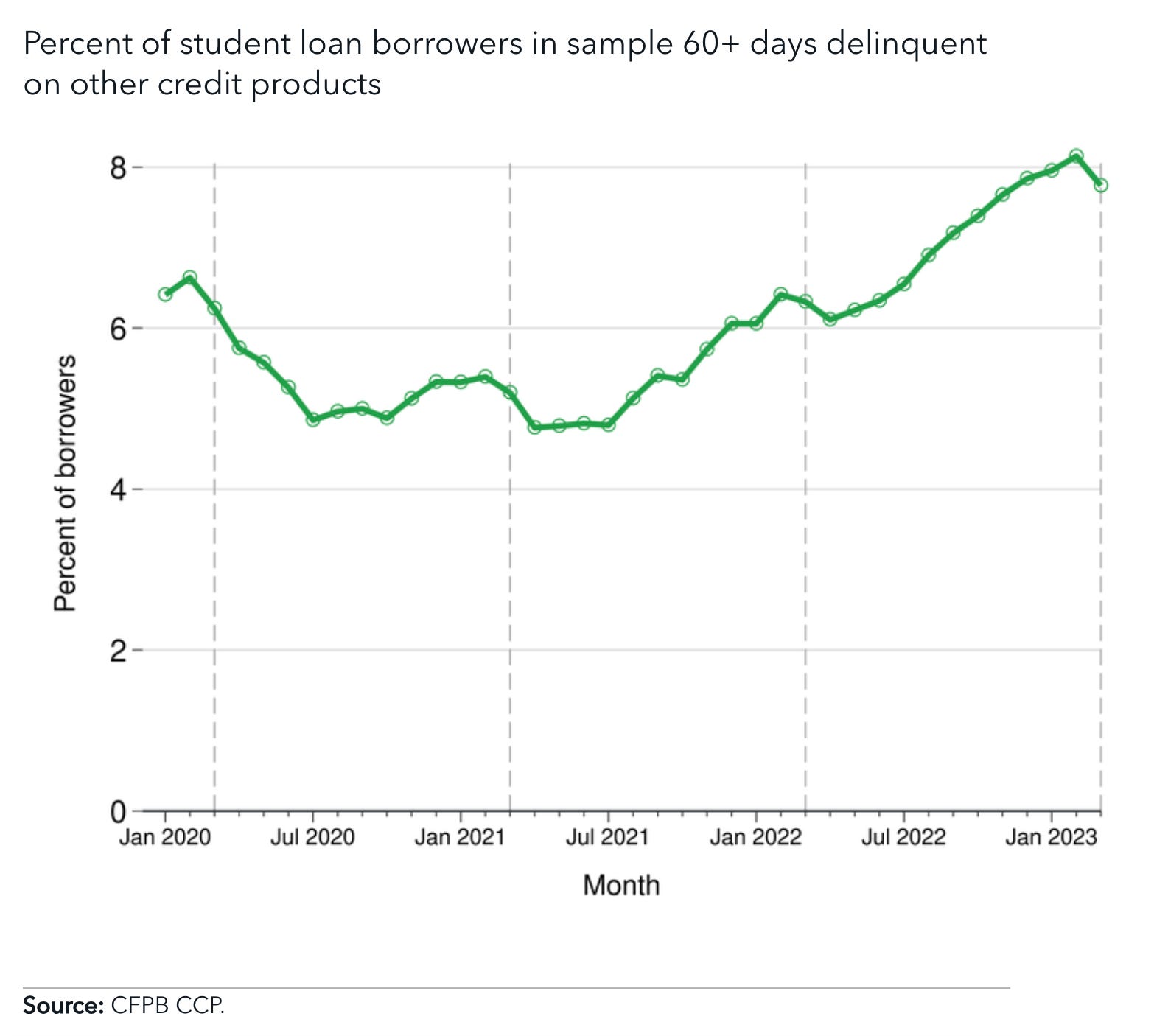

Ultimately, the system itself is in dire need of structural change, but something really has to be done about young people with pre-recession wages and ballooning student debt. One particularly sad outcome is watching the rising relationship between student debtors and those defaulting on other kinds of debt, which was recently explored by the Consumer Financial Protection Bureau.

I could make a lot of jokes here about how the payment restart will devastate the vintage pop-up scene and indie music festivals. Or restaurants like Lucien and Dimes. It’ll be a cultural shift, ha ha. But really, thousands of people – who held the reasonable expectation that the Biden Administration would follow through on its promise and adjusted their household finances accordingly – are now going to choose between not paying rent or defaulting on their loans this Fall. Are we really ready for that?

Now it seems my options are few. I could pay the “accrued interest” back in October and accept my loss. I could delay, and pray my servicer gets sued in a window which also allows for debt cancellation (tempting, however unlikely). Or I could sue them myself to right the wrong, likely paying more to hire an attorney than I would just paying it back. I will spend some time considering each option. But most likely I will sit at my desk, reach into my wallet with my insect-like fingers, and pay it off.

I always found this argument kind of funny, because the people with the inherited wealth and the cool jobs are the ones who do not have loans.